[This work is based on this course: Artificial Intelligence for Business.]

A company wants to implement a plan premium for its clients. The goal for this online reatail business is getting as many suscribers as possible to the special plan. This is offered for 100$ per year.

The marketing department has provided us 10 differents strategies and our IA will not have any idea which one is the best. So we will assume that each has a fixed conversion rate.

To simulate this Case Study, we will assume these strategies have the following conversion rates:

| Strategy | Conversion Rate |

|---|---|

| 1 | 0.01 |

| 2 | 0.08 |

| 3 | 0.1 |

| 4 | 0.04 |

| 5 | 0.26 |

| 6 | 0.12 |

| 7 | 0.17 |

| 8 | 0.09 |

| 9 | 0.19 |

| 10 | 0.25 |

We will simulate 10,000 clients being approached successively by one of the 10 strategies, and with the rewards matrix we will simulate the client’s decision to subscribe yes(1) or no(0) to the premium plan. As an example, the first few rows of a simulated reward matrix:

| 0 | 0 | 0 | 1 | 0 | 1 | 0 | 1 | 0 | 0 |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 |

| 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 |

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

Thompson sampling will collect the feedback from each of these subscribers and thanks to its powerful algorithm, it will quickly figure out the strategy with the highest conversion rate.

Thompson sampling steps:

We repeat for more than 10000 iteratios for each round C.

Step 1: A random value is chosen for each iteration i. This value has to follow the distribution:

,where:

is the number of times the i-th strategy has gotten a reward equal to 1 until the n-th round.

is the number of times the i-th strategy has gotten a reward equal to 0 until the n-th round.

Step 2: We select the strategy $s(n)$ that gives us the highest value

Step 3: We update

-

If the selected strategy

has a reward equal to 1:

.

-

If the selected strategy

.

Each strategy has its own beta distribution. Throughout the rounds, the beta distribution strategy with the highest conversion rate will progressively move to the right, and the beta distributions strategy with the lowest conversion rates will progressively move to the left (Steps 1 and 3). Therefore, due to Step 2, the strategy with the highest conversion rate will be selected.

[Source: https://medium.com/pursuitnotes/day-28-reinforcement-learning-3-7a98bacc0927]

We will also implement the random selection algorithm, which will select a random strategy each round. This will be our benchmark for evaluating the return of our Thompson sampling model. Of course, the Thompson sampling and the random selection algorithm will compete in the same simulation using the same reward matrix. Once the complete simulation is done, we will evaluate the Thompson Sampling return by calculating the relative return:

Import libraries

import numpy as np import matplotlib.pyplot as plt import random

Config Parameters

C = 100000 #Number of rounds = Number of clients s = 10 #Number of marketing strategies

Building the simulation

conversion_rates = [0.01, 0.08, 0.1, 0.04, 0.26, 0.12, 0.17, 0.09, 0.19, 0.25]

X = np.array(np.zeros([C, s]))

for i in range(C): #Rounds=clients

for j in range(s): #Strategy

if np.random.rand() <= conversion_rates[j]: #if our random number.....then...

X[i,j] = 1

Random assignment and Thompson sampling

strategies_selected_rs = [] #random select

strategies_selected_ts = [] #thompson select

total_reward_rs = 0

total_reward_ts = 0

number_of_rewards_1 = [0] * s #creating a s-zeros list

number_of_rewards_0 = [0] * s

for n in range(0, C): #Starting rounds=clients

# Random Selection

strategy_rs = random.randrange(s) #select a random strategy

strategies_selected_rs.append(strategy_rs)

reward_rs = X[n, strategy_rs] #WE get the reward which has been created before

total_reward_rs += reward_rs

# Thompson Sampling

strategy_ts = 0

max_random = 0

for i in range(0, s):

#Step 1

random_beta = random.betavariate(number_of_rewards_1[i]+1,

number_of_rewards_0[i]+1)

#Step 2

if random_beta > max_random:

max_random = random_beta

strategy_ts = i

strategies_selected_ts.append(strategy_ts)

#Step 3

reward_ts = X[n, strategy_ts]

if reward_ts == 1:

number_of_rewards_1[strategy_ts] += 1

else:

number_of_rewards_0[strategy_ts] += 1

total_reward_ts += reward_ts

Relative and absolute return

absolute_return = (total_reward_ts - total_reward_rs)*100 #We assume 100 $/sale.

relative_return = (total_reward_ts - total_reward_rs) / total_reward_rs * 100

print("Absolute Return: {:.0f} $".format(absolute_return))

print("Relative Return: {:.0f} %".format(relative_return))

Absolute Return: 1287500 $

Relative Return: 98 %

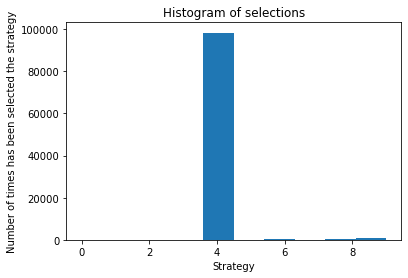

Plotting histogram

plt.hist(strategies_selected_ts)

plt.title("Histogram of selections")

plt.xlabel("Strategy")

plt.ylabel("Number of times has been selected the strategy")

plt.show()

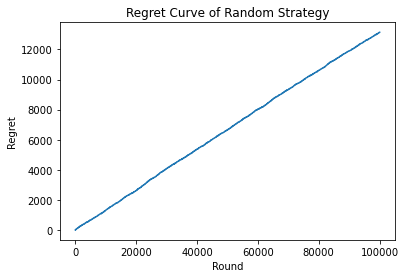

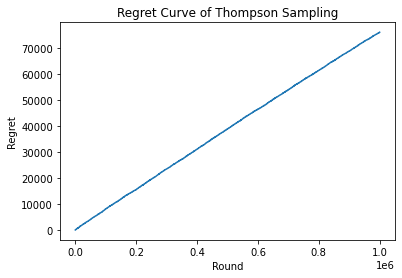

Regret Curve

The Regret curve is the representation of the difference between the best strategy and the model, with respect to the rounds. The best strategy is calculated obtaining the maximum accumulated rewards in all the different strategies in each round.

rewards_strategies = [0] * s

for n in range(0, C):

# Best Strategy

for i in range(0, s):

rewards_strategies[i] = rewards_strategies[i] + X[n, i]

total_reward_bs = max(rewards_strategies)

– Regret of Thompson Sampling:

strategies_selected_ts = []

total_reward_ts = 0

total_reward_bs = 0

numbers_of_rewards_1 = [0] * s

numbers_of_rewards_0 = [0] * s

rewards_strategies = [0] * s

regret = []

for n in range(0, C):

# Thompson Sampling

strategy_ts = 0

max_random = 0

for i in range(0, s):

random_beta = random.betavariate(numbers_of_rewards_1[i] + 1,

numbers_of_rewards_0[i] + 1)

if random_beta > max_random:

max_random = random_beta

strategy_ts = i

reward_ts = X[n, strategy_ts]

if reward_ts == 1:

numbers_of_rewards_1[strategy_ts] = numbers_of_rewards_1[strategy_ts] + 1

else:

numbers_of_rewards_0[strategy_ts] = numbers_of_rewards_0[strategy_ts] + 1

strategies_selected_ts.append(strategy_ts)

total_reward_ts = total_reward_ts + reward_ts

# Best Strategy

for i in range(0, s):

rewards_strategies[i] = rewards_strategies[i] + X[n, i]

total_reward_bs = max(rewards_strategies)

# Regret

regret.append(total_reward_bs - total_reward_ts)

– Plotting the Regret Curve of Thompson Sampling:

plt.plot(regret)

plt.title('Regret Curve of Thompson Sampling')

plt.xlabel('Round')

plt.ylabel('Regret')

plt.show()

– Regret of the Random Strategy:

strategies_selected_rs = []

total_reward_rs = 0

total_reward_bs = 0

numbers_of_rewards_1 = [0] * s

numbers_of_rewards_0 = [0] * s

rewards_strategies = [0] * s

regret = []

for n in range(0, C):

# Random Strategy

strategy_rs = random.randrange(s)

strategies_selected_rs.append(strategy_rs)

reward_rs = X[n, strategy_rs]

total_reward_rs = total_reward_rs + reward_rs

# Best Strategy

for i in range(0, s):

rewards_strategies[i] = rewards_strategies[i] + X[n, i]

total_reward_bs = max(rewards_strategies)

# Regret

regret.append(total_reward_bs - total_reward_rs)

– Plotting the Regret Curve of Random Strategy:

plt.plot(regret)

plt.title('Regret Curve of Random Strategy')

plt.xlabel('Round')

plt.ylabel('Regret')

plt.show()